Request a Demo

Customers Renew. But That Doesn’t Mean They’re Happy.

Most insurers treat renewal as success.

Policy renewed

Revenue retained

Customer stays

Everything looks good on paper.

But here’s the uncomfortable question:

→ Did the customer renew because they wanted to… or because they had no better option?

That difference defines your future churn.

Because:

- reluctant renewals leave next cycle

- dissatisfaction doesn’t disappear, it compounds

- one bad claim later can break the relationship

That is why a post renewal survey in insurance matters.

Not as a reporting exercise.

But as a way to understand the quality of the renewal decision.

What is a Post Renewal Survey in Insurance?

A post-renewal survey is a short feedback survey sent after a customer renews their policy to understand:

- why they chose to renew

- how confident they feel about that decision

- what concerns they had before renewing

- what almost stopped them

- what could improve their experience going forward

This is not a retention survey.

This is a decision validation system.

Why Post Renewal Surveys Matter More Than They Seem

Renewal does not mean satisfaction.

A customer can renew and still be:

- frustrated with support

- unclear about policy benefits

- unhappy with claim experience

- sensitive to pricing

- exploring competitors for next year

What Most Insurers Get Wrong About Renewals

Most renewal programs focus on process, not insight.

Common mistakes:

- assuming renewal = satisfaction

- not collecting feedback after renewal

- focusing only on price-driven retention

- ignoring renewal confidence

- not linking renewal feedback with claims experience

👉 This leads to a dangerous blind spot: customers who stay… but are already planning to leave.

Post Renewal vs Pre Renewal Survey: What’s the Difference?

| Survey Type | When It Is Sent | What It Solves |

| Pre-renewal survey | Before expiry | Predict churn and intervene |

| Post-renewal survey | After renewal | Understand why customer stayed |

| Post-claim survey | After claim decision | Measure trust after outcome |

| Onboarding survey | After purchase | Capture early experience |

👉 Pre-renewal tells you who might leave

👉 Post-renewal tells you why they stayed

To understand the full journey, insurers often combine this with an insurance onboarding survey (early experience) and a post-claim survey (moment of truth).

When Should You Send a Post Renewal Survey?

Timing matters.

Too early → no reflection

Too late → poor recall

Ideal Timing: Right After Renewal

This ensures the decision is still fresh, feedback is honest, and experience is recent.

Why Should You Use a Post-Renewal Survey (And When Not To)

Use a post-renewal survey if:

- you want to understand why customers stayed

- you see renewals happening but loyalty is unclear

- you suspect hidden churn in the next cycle

- you want to connect claims → renewal behavior

Avoid using it if:

- you’re only trying to predict churn (use pre-renewal instead)

- you don’t have a system to act on feedback

This ensures the survey drives action, not just data

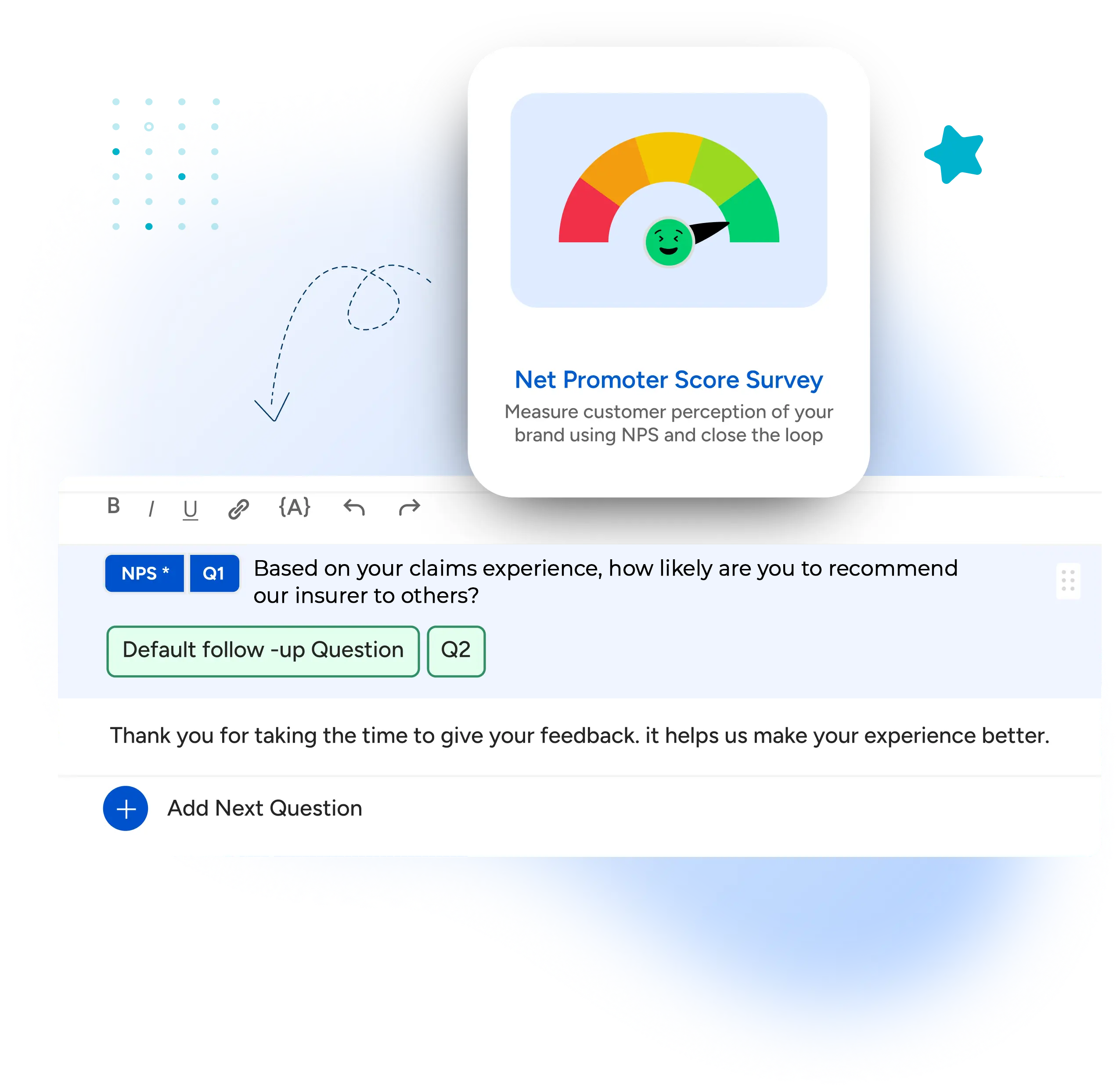

Which Metric Matters Most After Renewal?

- Use CES → to understand the ease of renewal

- Use NPS → to measure long-term trust

- Use open-ended feedback → to understand hesitation

Together, they tell you not just what happened, but why.

Best Questions for a Post-Renewal Survey in Insurance

Here’s a simple, effective post-renewal survey template insurers can use after a policy is renewed.

Keep it short, focused, and aligned to the decision reflection moment.

- How easy was the renewal process? (CES)

- What is the primary reason for the score you gave? (Open-Ended)

- Based on your overall experience, how likely are you to recommend our insurer to others? (NPS)

- How confident are you in your decision to renew your policy with us? (Renewal Confidence)

- Please rate the following aspects of your experience (Key Attribute Ratings)

- Clarity of policy coverage

- Value for premium paid

- Claims experience (if applicable)

- Customer support responsiveness

- Communication from the insurer

- Ease of the renewal process

- What almost stopped you from renewing your policy with us? (Open-Ended)

Note: A post-renewal survey should ideally be limited to 3–5 questions to ensure high response rates. If needed, rotate or prioritize questions based on your use case.

How to Identify Risk Even After Renewal

1. High-Risk Renewals (Renewed, But Likely to Churn Next Cycle)

These are the most critical customers to act on.

They have renewed – but the relationship is weak.

Key Signals

- Low NPS (0–6)

- Low renewal confidence

- Negative or emotional open-ended feedback

- Strong complaints about claims, pricing, or support

- Mentions of competitors or switching intent

- “Only renewed because…” type responses

What It Actually Means

👉 The customer did not renew out of trust

👉 They renewed due to inertia, dependency, or lack of alternatives

Examples You’ll See in Feedback

- “Premium is too high, will check other options next year”

- “Claim experience was not great”

- “I renewed because my agent told me to”

Action Required

- Immediate follow-up (within 24–48 hours)

- Retention or service recovery call

- Clarify concerns (pricing, claims, benefits)

- Track if intervention improves next-cycle retention

👉 These are saved customers – not loyal customers

2. Medium-Risk Renewals (Stable, But Easily Influenced)

These customers are not unhappy – but not committed either.

Key Signals

- Neutral NPS (7–8)

- Moderate confidence in renewal decision

- Price sensitivity

- Comparison behavior (“I checked other insurers”)

- Minor complaints or hesitation signals

What It Actually Means

👉 The customer is open to switching

👉 Your differentiation is not strong enough

Examples You’ll See

- “Everything is fine, but premium is slightly high”

- “I compared a few options before renewing”

- “Service is okay, nothing exceptional”

Action Required

- Strengthen value communication

- Reinforce benefits (coverage, claims, service)

- Improve engagement (proactive touchpoints)

- Reduce friction in future interactions

👉 These are competitive customers – not guaranteed renewals

3. Low-Risk Renewals (Confident and Loyal Customers)

These are your strongest customers.

Key Signals

- High NPS (9–10)

- High renewal confidence

- Positive open-ended feedback

- Strong satisfaction with claims and support

- No mention of competitors

What It Actually Means

👉 The customer trusts your insurer

👉 Renewal was a confident decision

Examples You’ll See

- “Very satisfied with the service”

- “Claims process was smooth and transparent”

- “Happy to continue with you”

Action Required

- Maintain experience consistency

- Leverage for referrals and advocacy

- Use feedback as proof points internally

- Protect this segment from future friction

👉 These are true retained customers – not just renewed ones

How Insurers Should Use Post Renewal Feedback

Collecting feedback is easy. Using it is where most programs fail.

A strong post-renewal program should connect:

👉 feedback → risk → ownership → action → outcome

1. Identify At-Risk Renewals (Immediately, Not Later)

Customers who renewed but show:

- low NPS

- low renewal confidence

- negative feedback

- price dissatisfaction

- claim-related frustration

These are your highest future churn risk customers

What Most Teams Do: Review this in monthly reports

What High-Performing Teams Do

- Flag instantly (real-time)

- Assign ownership (branch, RM, retention team)

- Trigger follow-up within 24–48 hours

→ Speed matters more than analysis here.

2. Detect Patterns Across Policies (Not Just Individual Cases)

Individual feedback helps you act. Patterns help you improve.

Over time, post-renewal feedback will reveal:

- products with weak perceived value

- regions with poor service experience

- branches with renewal friction

- premium segments with price sensitivity

- customers with prior claim dissatisfaction

Most teams look at: “What happened to this customer?”

Better teams ask: “Where is this happening repeatedly?”

That’s where real CX improvement comes from.

3. Feed Insights Back Into Customer Journeys

Post-renewal feedback is not just about renewal.

It tells you what needs fixing across the journey.

Use it to improve:

1. Onboarding

→ Customers didn’t understand the policy

Fix clarity and communication early

2. Claims Experience

→ Dissatisfaction during claims

Improve transparency and explanation

3. Communication

→ Low engagement or confusion

Strengthen proactive touchpoints

4. Pricing Perception

→ “Premium is too high”

Explain value better, not just price

👉 This is where insurers connect post-claim feedback (trust moment) with post-renewal feedback (loyalty validation)

4. Close the Loop (Even After Renewal)

Post-renewal is actually one of the best moments to strengthen the relationship.

When a customer says, “I’m not fully confident”

You should:

- follow up

- clarify concerns

- explain coverage

- reassure value

This turns: reluctant renewal → confident renewal

And that directly impacts next-cycle retention.

What a Good Post Renewal Survey Program Looks Like

By now, the strategy is clear.

Now comes execution.

A strong post-renewal survey program should be able to:oo

- trigger surveys automatically after policy renewal

- capture renewal confidence along with NPS

- collect open-ended feedback to understand hesitation

- segment results by product, region, branch, agent, and premium band

- identify hidden churn risk even after renewal

- detect pricing and claim-related dissatisfaction

- alert teams on low-confidence responses

- assign ownership for follow-up

- track resolution before the next renewal cycle

👉 This is where most programs break – not in collecting feedback, but in acting on it – — which is where having the right insurance customer feedback software becomes critical.

How to Run a Post-Renewal Survey (Simple Steps)

- Trigger survey 3–7 days after renewal

- Ask NPS + renewal confidence + open-ended question

- Identify high-risk responses instantly

- Assign follow-up to relevant team

- Track whether issue is resolved

- Analyze patterns across segments

👉 This ensures feedback leads to action, not just reporting

How This Looks in Practice

👉 By this point, the strategy is clear.

The real challenge is executing this consistently across thousands of policies.

To do this, teams need a system that can:

- trigger surveys automatically after renewal

- identify risk based on scores and feedback

- assign ownership to the right teams

- track whether action actually happened

This is where platforms like SurveySensum act as the execution layer.

1. Build the Post-Renewal Survey

Create a short, focused survey aligned to the renewal decision moment:

- NPS as the trust indicator

- renewal confidence as the primary signal

- value perception question (premium vs benefit)

- key experience drivers (claims, support, communication)

- open-ended feedback to capture hesitation

👉 This ensures you measure not just renewal – but quality of renewal

2. Trigger Surveys After Renewal

Instead of manual sending, surveys can be triggered automatically after:

- policy renewal confirmation

- premium payment completion

- renewal acknowledgment communication

This ensures feedback is captured when:

- the decision is fresh

- the experience is still top of mind

3. Track Renewal Quality Across Segments

Once responses start coming in, teams can track:

- renewal confidence distribution

- NPS by product, region, and branch

- performance by agent or partner

- premium band-based dissatisfaction

- claim vs non-claim customer differences

👉 This helps identify where customers renew confidently vs reluctantly

4. Analyze “Why Customers Hesitated”

Scores alone are not enough.

SurveySensum’s text analytics tool can group feedback into themes like:

- pricing concerns

- claim dissatisfaction

- unclear policy benefits

- weak communication

- agent dependency

- comparison with competitors

👉 This is where you uncover hidden churn drivers

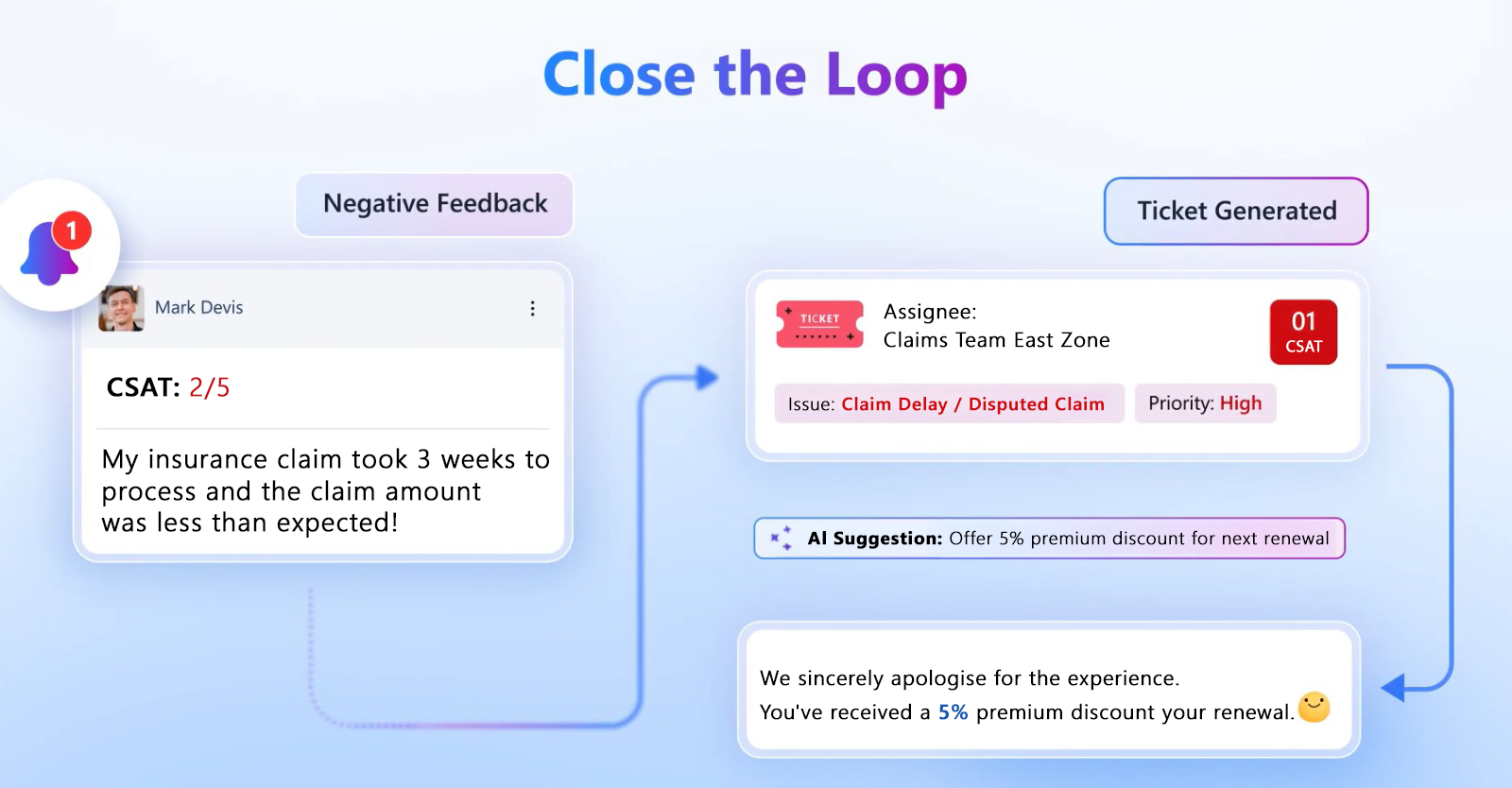

5. Identify and Act on High-Risk Renewals

How This Works in Reality

A customer renews but gives:

- NPS: 5

- Confidence: Low

- Comment: “Premium is too high”

The system:

→ flags the response instantly

→ assigns it to the retention team

→ triggers a follow-up call

👉 This is how feedback turns into action – immediately, not next quarter.

6. Close the Loop and Track Outcomes

Feedback should not stop at analysis.

This allows teams to:

- track follow-up status

- monitor whether the issue was resolved

- ensure accountability across teams

- measure improvement over time

👉 This is where feedback becomes actionable, not just informational

What This Enables

With a structured post-renewal program, insurers can:

- detect dissatisfaction immediately after renewal

- understand why customers renewed (or hesitated)

- act on high-risk cases before next renewal cycle

- improve long-term retention, not just renewal rates

- align onboarding, claims, and renewal insights into one system

👉 Instead of manually running surveys and analyzing feedback, insurers can automate post-renewal programs and act on them in real time. Here’s how this works in practice →

A Simple Way to Think About It

A post-renewal survey should answer:

- Did the customer renew confidently?

- What nearly stopped them?

- Are they at risk next cycle?

- Who should act on it?

- What should we fix before the next renewal?

If your system cannot answer this – you are tracking renewals, not improving them

Final Thought

Most insurers measure renewal rates.

The best insurers measure renewal quality.

Because a customer who renews reluctantly… is just a churn case delayed.

FAQs: Post Renewal Survey in Insurance

What is a post renewal survey in insurance?

A post-renewal survey is sent after policy renewal to understand why customers stayed and whether they are at risk of leaving in the future.

When should a post renewal survey be sent?

Ideally within 3–7 days after renewal when the decision is still fresh.

Should insurers use NPS after renewal?

Yes, but combine it with renewal confidence and open-ended feedback for better insight.

Why is post renewal feedback important?

It helps detect hidden dissatisfaction and future churn risk, even among customers who have already renewed.

👉 Want to see how insurers track renewal confidence, identify silent churn risk, and act on feedback before the next renewal cycle?

Explore how post-renewal workflows actually work →

Free Forever • No Feature Limitation • No Credit Card Required • Sign Up For Free ![]()

Increase ROI by 3x with targeted feedback & analysis

Boost Customer Satisfaction by up to 20%

Reduce Churn by identifying pain points in real time

See it in Action

Contents

How much did you enjoy this article?